The civil aviation market in the world. Boeing Market Forecast

Aircraft industry implies the design and creation of a full-fledged aircraft and its components. A few and very expensive products are subsequently used for both civilian and military purposes.

There is no doubt that the most convenient way to travel is by plane. About significance aircraft in the affairs of the country's defense and there is no need to speak. All this makes the aviation industry a priority and singles out the largest aircraft manufacturing companies in the world in a special category.

Giants of the aircraft industry

In the aircraft industry today, almost all engineering products are used. In addition, all innovative scientific and technical processes find undoubted application in it. It is logical to assume that if the state is able to locate such an industrial complex on its territory, this means its financial solvency, the opportunity to show itself as a reliable business partner.

Direct aircraft rental can be an interesting idea for a startup. A striking example of such a business is described.

The constant development of the industry involves the use of super-new information technologies (we are talking not only about the manufacture of aircraft, but also the components for them). From the economic point of view, this is, of course, certain and very serious financial investments. On the other hand, every state needs the aviation industry. This formulation of the question makes it necessary for such enterprises to receive assistance from the state.

Below is a list of the ten largest aircraft companies in the world. The Forbes rating was based on the market value of enterprises, which “placed” them in their places in the top 10.

| Place in general list Forbes | Name of company | Location country | Market value for 2016, billion dollars |

|

|---|---|---|---|---|

| Rolls-Royce Holdings | Great Britain | |||

| Great Britain | ||||

| Northrop Grumman | ||||

| General Dynamics | ||||

| Netherlands | ||||

| The Boeing Company |

10th Place: Starting with Rolls-Royce Holdings

A division of the company with a big name specializes in the production of engines for civil aviation. The organization has been operating in the aircraft industry since 1904. For more than a century of history, the corporation has earned worldwide recognition and the desire to cooperate with foreign customers. In this regard, Russia is not far behind: it is Rolls-Royce that offers to supply its engines for the future Russian-Chinese long-haul airliner.

The company employs 54,100 people. Annual revenue last year was $20.18 billion.

9th place: French company Thales

The 20.6 billion capital value of this company is deservedly due to the conscientious work that dates back to 1918. Today the organization is engaged in the release of information systems of aerospace significance. Among the company's products are components for military aviation, electronics for fighter jets.

The organization bears the name of Thales of Miletus, an ancient Greek philosopher. Offices are located in more than 50 countries of the world, and the total staff of all employees working in it reaches 68,000 people. Sales revenue for 2016 amounted to $16.5 billion.

8th place: British company BAE Systems plc

BAE Systems is essentially a British defense company that promotes its products in the aerospace industry. It works with foreign customers (mainly from the USA) through its subsidiary BAE Systems Inc. The division of British Aerospace (BAe) works directly with the aerospace environment.

The organization actively lobbies its interests in the former Soviet republics. For example, since 2001 it has owned 49% of the national Kazakh carrier Air Astana.

According to the latest data, the organization employs 88,200 people worldwide. The headquarters itself is located in London. Now about the financial component: in 2016, the corporation's revenue amounted to $24 billion.

7th place: French corporation Safran

Aerospace and aeronautical equipment are among the several focus areas of this French industrial conglomerate. The main focus is on commercial and military engines, as well as the restoration and repair of jet engine models. There is also a turbo direction - turboshaft engines for helicopters and turbines for rockets. In addition, other components for aircraft and engines are also manufactured.

In total, the company employs 57,495 people. Revenue for 2016 was $18.23 billion.

6th: Northrop Grumman Corporation (NOC)

This corporation was organized in 1994 and combined Northrop Corporation and Grumman Corporation. Aviation and space are not the only areas of its activity. As a technique for this, the company produces military fighters and even airships (Airlander 10).

Northrop Grumman Corporation received the equivalent of $24.51 billion in 2016 revenue. In total, this organization employs 67,000 people.

5th place: Raytheon

The top five starts with the American manufacturer, which receives more than 90% of its income from defense orders. The products are of a rather specific nature - these are radio-controlled missiles and guidance systems, components of space systems, guidance technologies.

The name Raytheon is interestingly translated - “Divine Ray”, which is associated with the initial production of ray tubes since 1922. In an enterprise related to aviation, Raytheon retrained already during the Second World War. The project was the development of protection against Japanese kamikaze attacks, which turned into large-scale production.

To date, Raytheon Corporation employs 63,000 people. Revenue for 2016 was $24.07 billion.

4th place: American General Dynamics

One of the giants in the production of military and aerospace technical arsenal is the fifth on the planet in terms of concluding contracts related to the supply of precisely aircraft for defense needs.

The organization is a supplier of the most powerful information systems, which include intercontinental missiles, satellite data processing systems and similar equipment. For a long time, General Dynamics collaborated with NASA.

In addition to aerospace products, the company is also engaged in the production of marine and combat systems. The leading role here lies in the development of information technology. In total, the organization employs 98,800 employees who provided revenue of $31.35 billion in 2016.

3rd: Bronze Dutchman Airbus Group (former EADS)

The organization today is better known under the name Airbus Group. It is the largest aerospace corporation in Europe, headquartered not only in the Dutch capital, but also in Paris and Ottobrunn.

The company is relatively young, formed by the merger of other large specialized organizations in 2000. The renaming of EADS to Airbus Group happened only in 2013. At the same time, the management announced a restructuring, after which three divisions are expected: Airbus will be engaged in the direction of commercial aircraft construction, Airbus Helicopters will specialize in the production of helicopters, and Airbus Defense & Space will become a site for the production of military and space equipment.

The company's revenue for 2016 amounted to $73.7 billion. 133,000 people work for the benefit of the Airbus Group.

2nd Place: Lockheed Martin Silver Medalist

Lockheed Martin Corporation is a global company that specializes in the defense and space market segment. Notable production examples include fighter-bombers (5th generation F-35) and F-22 class fighter models.

The main client of the company is the native American government, which brings in approximately 82% of the revenue. The rest is provided by international contracts (work under the arms sales program). The number of commercial orders is only 1% of revenue. The company's full profit for 2016 is $79.9 billion.

In total, this organization employs 97,000 people. The headquarters is located in the US state of Maryland, in the city of Bethesda.

1st place: the undisputed leader of Boeing

This world's largest manufacturer is headquartered in Chicago. Specialization - production of aviation, military and even space technology. The military arsenal is handled by the Boeing Integrated Defense Systems division, while the civilian direction is under the wing of Boeing Commercial Airplanes.

In addition, one of the largest aircraft manufacturing companies in the world produces a wide range of military equipment (including helicopters) and participates in large-scale space programs (an example is CST-100, a spacecraft).

The capitalization of the company is 108.9 billion dollars, and the revenue for the past year is 94.6 billion dollars. Today, this structure employs 150,500 people. Factories operate in 67 countries of the world, and the delivery of goods goes to 145 countries. And that's not all the numbers: more than 5200 suppliers from 100 countries are partners of the organization.

Features of the aircraft industry

Initially, the aircraft industry was formed as an industry of a military nature. The issue of civilian objects began to be thought about later. This made the aircraft industry monetized and gave certain specific features:

- The production of military products is determined by the military orders of their own state and the possibilities of export world supplies.

- The production of civil aircraft depends entirely on the receipt of national and world orders. Naturally, these figures can fluctuate greatly depending on demand.

The production of airliners may well become a program of domestic import substitution. Learn more detailed information you can in this article.

A separate issue concerns the cost of production itself. It may surprise you that back in the mid-1990s, it was estimated at 4 times less than the automobile one, that is, at only $250 billion. Everything is explained simply: aircraft cannot be called a mass commodity, this is a piece production. The annual production of civil aviation facilities hardly exceeds 1,000 pieces, while the figures for the military structure can be even lower, only 600 pieces per year.

The situation is somewhat saved by the well-established production of so-called light aircraft. The great demand for them is also due to an affordable price - from 20 to 80 thousand dollars. Most often, such products are used for educational, sports or business purposes.

The high science intensity of the whole process is also of great importance. Usually, the development of any aircraft (both military and civilian) can take from 5 to 10 years. The high prices for the design and creation of aircraft facilities are so high that few firms in the world can afford such activities:

Position in the Russian market

The leader of the domestic aircraft industry is the United Aircraft Corporation (UAC). It was established in 2006 and united all previously existing aircraft design organizations in the country.

The corporation's revenue is 295 billion rubles. During the work, more than 200 aircraft were delivered. In recent years, special emphasis has been placed on the development of the short-haul line Sukhoi Superjet 100 (SSJ100). In 2016 alone, 34 deliveries of this aircraft model took place. To date, more than 50 such machines are in operation, and 13 of them are used outside of Russia.

Aircraft building in Russia can be considered as an object of venture business. Read more about this concept.

Another promising direction of the UAC is the medium-haul airliners of the new generation of the MC21 brand, the first flight tests of which took place last year. There is a demand for them: immediately after the tests, 175 orders and applications for the manufacture of such equipment were received. The UAC plans to produce 72 such airliners a year.

10

10th - Pakistan

Fighters Bombers Transport aircraft combat helicoptersThe Royal Pakistan Air Force was formed in 1947. The Pakistan Air Force actively participated in the wars with India, and during the Afghan war they intercepted Soviet and Afghan aircraft invading the country's airspace. Pakistan buys aircraft mainly from American and Chinese production. The Air Force has 65,000 soldiers and officers (including 3,000 pilots). The state has about 955 combat, transport and training aircraft.

9

9th place - Turkey

Fighters Bombers Transport aircraft combat helicoptersThe Turkish Air Force was founded in 1911. By 1940, Turkey had the largest air force in the Middle East and the Balkans. The Turkish air force participated in the invasion of Cyprus (1974) and in military operations in the Balkans in the 1990s, and is also periodically involved in military operations inside the country. The number of personnel is about 60,000 people. The development of its own fifth-generation fighter TF-X is underway.

8

8th place - Egypt

Fighters Bombers Transport aircraft combat helicoptersThe Egyptian Air Force was created on November 2, 1930 by the decree of King Fuad I. Egyptian aviation took an active part in the Arab-Israeli wars. In the 1950s-1970s, the Soviet-made aircraft were mainly in service. After breaking off relations with the USSR, Egypt began to purchase aircraft from the United States and France. The number of troops is about 40 thousand people.

7

7th place - France

Fighters Bombers Transport aircraft combat helicoptersCreated as part of the French army in 1910. The French Air Force actively participated in the First and Second World Wars. After the occupation of the country by Germany in 1940, the national air force split into the Vichy Air Force and the Free French Air Force. Main producer aviation technology- Dassault Aviation. It is engaged not only in the creation of military types of aircraft, but also regional and business class. Second in size Airbus S.A.S manufactures cargo, military transport and passenger vehicles.

6

6th place - South Korea

Fighters Bombers Transport aircraft combat helicoptersThe basis of weapons are American-made aircraft and helicopters, but the government South Korea Significant efforts are being made to organize the production of their military equipment and reduce dependence on the United States in military and economic terms. There is also a certain amount of aircraft of Russian, English, Spanish and Indonesian production in service. In terms of the number of aviation equipment and the number of personnel, the South Korean Air Force is more than twice inferior to the North, but it is armed with more modern equipment, and the average flight time of pilots is higher. Since 1997, female cadets have been enrolled in the Air Force Academy. The number of staff is about 65 thousand people.

5

5th place - Japan

Fighters Bombers Transport aircraft combat helicoptersThe Japan Air Self-Defense Force was established in 1954. Until the end of World War II, aviation was directly subordinate to the imperial army and navy of Japan. It was not singled out as a separate type of troops. After the Second World War, during the formation of new armed forces, the Japan Air Self-Defense Force was formed, which was armed with US-made aircraft. After the United States refused to sell the F-22 fifth-generation fighter to Japan in 2007, the Japanese government decided to build the Mitsubishi ATD-X, its own fifth-generation aircraft. On the this moment the number of personnel is 47,123 people.

4

4th place - India

Fighters Bombers Transport aircraft combat helicoptersAir Force India were created on October 8, 1932, and the first squadron appeared in their composition on April 1, 1933. They played an important role in the fighting on the Burmese front during World War II. In the years 1945-1950, the Indian Air Force carried the prefix "royal". Indian aviation took an active part in the wars with Pakistan, as well as in a number of smaller operations and conflicts. For 2017, the number of personnel is 127,000 people.

3

3rd place - China

Fighters Bombers Transport aircraft combat helicoptersThe PLA Air Force was established on November 11, 1949 after the victory of the Chinese Communist Party in civil war. The Soviet Union played a major role in their creation and armament. Since the mid-1950s, the production of Soviet aircraft at Chinese factories began. The Great Leap Forward, the severance of relations with the USSR, and the "cultural revolution" caused serious damage to the Chinese Air Force. Despite this, in the 1960s, the development of their own combat aircraft began. After the end of the Cold War and the collapse of the USSR, China began to modernize its Air Force, purchasing multifunctional Su-30 fighters from Russia and mastering the licensed production of Su-27 fighters. Later, China broke the contract for the supply of Russian fighters and began to produce its own aircraft based on the know-how received. The number of personnel is 330,000 people.

2

2nd place - Russia

Fighters Bombers Transport aircraft combat helicoptersSince 1998, they have been a new type of Russian Armed Forces, formed as a result of the unification of the Air Force (Air Force) and the Air Defense Forces (Air Defense). Air force bases and brigades of aerospace defense troops form the basis of the combat strength of the Air Force. During the war years, 44,093 pilots were trained. 27,600 died in combat: 11,874 fighter pilots, 7,837 attack pilots, 6,613 bomber crew members, 587 reconnaissance pilots and 689 auxiliary pilots. After the collapse of the USSR in December 1991, the USSR Air Force was divided between Russia and other former Soviet republics. As a result of this division, Russia received approximately 40% of the equipment and 65% of the personnel of the Soviet Air Force, becoming the only post-Soviet space a state with long-range strategic aviation. Many planes were transferred from the former Soviet republics to Russia. Some were destroyed. In particular, 11 new Tu-160 bombers located in Ukraine were disposed of in cooperation with the United States.

In January 2008, Air Force Commander-in-Chief A.N. Zelin called the state of Russia's aerospace defense critical. In 2009, the purchases of new aircraft for the Russian Air Force approached the purchases of Soviet-era aviation. The fifth-generation fighter PAK FA is being tested; on January 29, 2010, its first flight took place. The entry into the troops of the 5th generation fighters is planned for 2020. The number of personnel is 148 thousand people.

1

1st place - USA

Fighters Bombers Transport aircraft combat helicoptersIn terms of the number of personnel and the number of aircraft, they are the largest air force in the world. AT modern form The US Air Force was formed on September 18, 1947, shortly after the end of World War II. Until that moment, they were part of the US Army. The number of personnel is 329,638 people.

The US Air Force ensures the high mobility of the US armed forces. In this component, not a single army in the world comes even close to the United States. The Air Force is a special type of force for the United States, which includes two components of the strategic triad at once: intercontinental ballistic missiles (ICBMs) and strategic aviation. It is the US Air Force that is a kind of pole of attraction for most of the innovations that the Americans are actively using in the military industry.

beneficial effect on her aviation market . Demand for new aircraft has noticeably revived, as one of the main problems of airlines continues to be an outdated fleet of aircraft. It is expected that in the coming years more than 1,000 aircraft of European and domestic (including those manufactured in the CIS countries) production will be purchased.

The leaders of world aircraft production (Airbus and Boeing) predict two types of development of air passenger transportation. According to the vision of Airbus specialists, a hub-and-spoke model (hubs and spokes) will be implemented, which essentially means the following. From the airports of the regions, by medium and small planes, passengers get to a large hub, from where long-distance flights to similar centers of the world are carried out.

Boeing analysts see a different development path, offering a point-to-point model, that is, a passenger gets to their destination with minimal transfers. Both companies presented long-haul aircraft projects to the market, allowing the proposed models for the development of air travel to be realized.

The Russian aviation market implements both models. Within the country, the number of point-to-point flights will inevitably increase, and hub-and-spoke flights will be operated international flights. Already, the demand for wide-body aircraft is growing, and the demand for long-distance international flights, according to experts, will grow up to 5% annually over the next 15-18 years. The growth of citizens' incomes, the liberalization of transport laws and the reduction in the cost of services will also affect the domestic aviation market, which will also grow.

Current situation and near future

As of today, about two hundred airlines operate in Russia. However, by 2025, only a couple of dozen successful ones will remain. Small regional companies continue to go bankrupt, as most of their pairs are obtained from obsolete (still Soviet) aircraft, which have practically exhausted their flight resource. And such companies are not able to afford to buy new equipment, and will be forced to leave the aviation market.

As of today, about two hundred airlines operate in Russia. However, by 2025, only a couple of dozen successful ones will remain. Small regional companies continue to go bankrupt, as most of their pairs are obtained from obsolete (still Soviet) aircraft, which have practically exhausted their flight resource. And such companies are not able to afford to buy new equipment, and will be forced to leave the aviation market.

Only large network air carriers can count on future success. They are still successfully operating today, they have an established network of routes that are profitable and familiar to passengers, and they have programs for updating the fleet of vehicles. Among the successful airlines that represent the country's aviation market are Aeroflot, S7, UTair, AiRUnion, Transaero and some others. The share of passenger traffic of each by 2020 will be at least 10 million people annually. It is possible that close companies may consolidate in the future, which will allow them to obtain considerable advantages and profitably purchase new aircraft.

Even now, the most successful Russian airlines are abandoning the secondary aircraft market, purchasing the latest developments of aircraft manufacturers on a par with the world's leading airlines. The only drawback for the aviation market and the domestic economy as a whole is that the Russian aviation industry will not be able to present a worthy competitive aircraft for medium-haul flights earlier than in 10-12 years (with the possible exception of the Sukhoi SuperJet).

How will the regional air transportation market change?

It is in the domestic aviation market of regional transportation that many experts see the future of aviation. Here, the main competitor continues to be the railway: cheaper, easier, no passport and face control required, no advance registration required. However, it is expected that over time, the price of air tickets will become closer to the railway and more affordable, and security measures will also be tightened at the stations. Of course, even the rise in price railway tickets will leave their positions profitable by 20-30%, but the absolute advantage railway will leave.

It is in the domestic aviation market of regional transportation that many experts see the future of aviation. Here, the main competitor continues to be the railway: cheaper, easier, no passport and face control required, no advance registration required. However, it is expected that over time, the price of air tickets will become closer to the railway and more affordable, and security measures will also be tightened at the stations. Of course, even the rise in price railway tickets will leave their positions profitable by 20-30%, but the absolute advantage railway will leave.

If taking the train becomes not much more convenient than going through the control on the plane, and the price of tickets is comparable, then many passengers will eventually prefer the planes. Their undoubted advantage in the speed of travel to the right place is undeniable. It is from this moment that short-range air transportation by small aircraft will spur the Russian aviation market, when half-forgotten flights between neighboring cities and regions return.

There is hope that the expected gigantic potential of the domestic air transportation market will prevent the authorities from handing it over to foreign carriers. Today they do not have access to the domestic aviation market, there is an agreement at the intergovernmental level that regulates air transportation between Russia and other countries. The number of flights is clearly fixed and even a specific carrier from the country is determined. The leading position is occupied by Aeroflot, which has the authority of the carrier on most foreign routes. However, after joining the WTO, it will not be easy for him to maintain his position.

General characteristics of the world market

Growth prospects for the civil aviation market are highly dependent on rising aviation fuel prices and the average annual growth rate of the global economy and trade. With an average annual growth rate of the world economy in 2007-2025. at the level of 3.1% per year, the average annual growth in the volume of air passenger transportation for the same period will be 4.9%, and cargo transportation - 6.1%. Then, according to the predictive estimates of the Boeing Co., the volume of the market for new civil aircraft in 2007-2025. will be about 2.6-2.8 trillion. USD In the period up to 2025, airlines will need approx. 28,600 new passenger and cargo aircraft. The global fleet of civil aircraft will more than double from 17,330 aircraft (2005) to about 36,000 (2025). Basically, these will be narrow-body (100-240 passengers) and wide-body (200-400 passengers) aircraft. 9,580 new aircraft will replace less efficient aircraft being withdrawn from the company's fleets. Most of them will be decommissioned, but 2220 passenger liners will be converted into cargo aircraft. In addition, airlines will receive 770 new cargo aircraft.

Aircraft in this segment, such as the Boeing 787 and Boeing 777, will enable airlines to grow successfully by operating more flights to more airports to meet passenger demand. Boeing-747 class and larger aircraft will be actively used on routes connecting Asian countries with other regions, as well as on transatlantic routes. The market is forecast to have strong demand for high-capacity cargo aircraft due to their high cost-effectiveness, reliability, range and excellent load factor performance.

By 2015, the number of 30-60-seat aircraft operated in the world will slightly exceed the 2000 units available in 2005, and by 2025 it will amount to 2500 units. At the same time, the number of cars with 61-90 seats will increase from the current 700 to 1,700 in 2015 and 3,300 in 2025. Demand for cars with a capacity of 91 to 120 passengers will expand at the fastest pace. If in 2005 there were just over 700 of them in the world's airlines, then by 2015 the fleet of such aircraft will increase to 2500, and by 2025 - up to 3800 units. In total, by 2025, 7,950 aircraft with a capacity of 30-120 passengers will be sold in the world for about $180 billion.

The business jet market is growing rapidly and will continue to expand in the medium term. In 2005, 737 business aircraft were sold worldwide, in 2006 850 were delivered, and in 2007 (according to preliminary estimates) the expansion of sales approached the level of 1000 aircraft. For the period 2008-2010. the total volume of orders is estimated at the level of 3.1-3.4 thousand aircraft. The main customers will be North American companies (61% of orders), which should upgrade their fleet of business jets by 23%. Strong demand is expected from European countries, and it will expand as a result of rising incomes of the population of Russia and Eastern Europe. By 2011-2012 a jump (up to 50% compared to the current level) of orders from Asia, Africa and the Middle East is predicted.

In total, between 2007 and 2025, about 24,000 business class aircraft will be produced worldwide.

According to Boeing Co. forecast, by 2026 airlines will acquire:

3,700 regional jets (less than 90 seats);

17,650 narrow-body aircraft (90-240 passengers in a two-class configuration);

6290 wide-body aircraft (200-400 passengers with a three-class layout);

960 Boeing-747 class aircraft and larger capacity (over 400 passengers in a three-class layout).

Geography of world production and consumption

The global civil aviation market is currently provided mainly by the products of four companies: the long-haul aircraft market is the area of interest for Boeing (USA) and Airbus (EU), and the vast majority of deliveries of regional aircraft are provided by Bombardier (Canada), Embraer (Brazil) and ATR ( Italy). Positions in the indicated market of other aircraft manufacturing enterprises of the world, including Russian ones, at the moment can be characterized as starting ones.

In 2006, the world leaders in the civil aviation industry produced ~820 mainline and ~250 regional aircraft of all types.

The largest market in the period 2006-2025. will be the countries of the Asia-Pacific region - 36% of the total amount of 2.8 trillion. dollars, which is due to the significant demand for wide-body airliners in the region. Airlines from North America will account for 28% of purchases, Europe - 24%. The remaining 12% comes from customers in Latin America, the Middle East and Africa.

An additional operational factor for the Asian market compared to the American and Western European markets is the presence of large passenger flows with a short length of airlines. With a large market volume, this feature can lead to the appearance of modifications or types of aircraft designed specifically for the countries of the Asia-Pacific region.

The number of aircraft manufacturing countries is expected to expand. The traditional players in the long-haul aircraft market, the European aviation industry, the American Boeing Corporation, will face competition from Russian (UAC), Asian manufacturers (AVIC-I, Mitsubishi HI), as well as long-haul aircraft projects created by companies that are traditional representatives of the regional and business markets. aviation (by Bombardier and Embraer). The market for jet regional aircraft will also acquire a multipolar supply due to falling into the sphere of interests of the aviation industry of developing countries. In addition to the traditional players represented by Embraer and Bombardier, which currently share the market almost on parity, the Russian SSJ-100 and the Chinese ARJ-21 may enter the market in the near future.

New products and technologies

The main trends in the technological development of the civil aircraft industry for the period up to 2025 include the following areas:

development of environmentally friendly power plants (providing a margin of 15 EPNdB in terms of noise, as well as a 20% reduction in emissions of harmful substances);

improvement of the consumption characteristics of civil aviation aircraft (by an average of 20%);

improvement of the aerodynamics of the airframe (search for alternative layouts, implementation of the concept of the carrier fuselage);

implementation of the concept of a fully electric aircraft (development of engines with an integrated electric generator, electrical control systems for aerodynamic surfaces, an autonomous air conditioning system, electric mechanisms for retracting and retracting the landing gear, restandardization of the onboard electrical system);

"black plane" - a constructive and technological solution to the problems of manufacturing an aircraft structure from light composite materials (for example, with carbon reinforcement);

the use of nanotechnologies to control the boundary layer, solve problems of increasing the strength of structures (nanomaterials), interactive diagnostics and taking readings of pressure, temperature, deformations, etc. (nanosensors);

global implementation of digital flight and navigation aids using satellite navigation systems.

Dear colleagues!

On behalf of the United Aircraft Corporation, we present a long-term forecast for the development of the civil commercial segment. This is an important event for us, because the expectations of the market, the vector of direction and the development of airlines are the message for us that we are trying to take into account when creating a line of aircraft.

UAC in the current period of time is going through a period of formation and strengthening in the market. You know that aircrafts in almost all segments from 30 seats have appeared in our product line. We understand that in order to occupy a worthy niche in the civil aviation market, it is extremely necessary and necessary to be competitive not only within Russian Federation but also in the foreign market.

We try to take into account the requirements of airlines, their expectations, not only in the appearance of aircraft, but in their technical specifications. The total market size until 2035 is estimated at about 6 trillion dollars, 42,000 aircraft dimension from 30 seats. And as I said, UAC currently has projects in almost all directions, with varying degrees of readiness.

First of all, this is the Sukhoi SuperJet 100. Now about 100 aircraft have been delivered, which are operated in Russia, Europe, Latin America, South-East Asia. Yesterday STLC under the Sukhoi SuperJet 100 program. For us, this is an extremely important event, as she plans to revive regional transportation in the south of Russia, based at the Rostov airport. We will also sign to increase the fleet of aircraft for the period 2020-2021 in addition to those that Azimuth will receive under the contract in 2017-2018 - this is 8 aircraft.

In the narrow-body aircraft segment, which is the most competitive market, you know that we have the MS-21 project. The aircraft made its first flight in May of this year, and is now undergoing flight and certification tests. The first deliveries will be in 2019, according to our expectations, this is a worthy competitor, which will take worthy place in the fleet of narrow-body aircraft. Of the large aircraft, we have a project with COMAC - this is ShFDMS. We have registered a joint venture. Active work is underway with Chinese partners, the technical appearance of this aircraft, its characteristics and the family of ShFDMS aircraft (wide-body long-haul aircraft) have been agreed. A joint venture has been registered, active work is underway with Chinese partners, the technical appearance of the aircraft, characteristics, family are being coordinated, and now we are at the stage of the beginning of preliminary design.

In the segment of regional aircraft - turboprop Il-114. That year, as you know, a decision was made to launch the Il-114-300 program. The first flight of the aircraft is expected in 2018, deliveries in 2021. Within the framework of MAKS there will be a second conference with operators, I hope that the aircraft will fully meet the expectations of regional companies and we will try to take into account their requirements.

That's all I wanted to say. I give the floor to Tamara Kakushadze, Vice President for Marketing " civil aircraft Dry".

Thank you for your attention!

Good afternoon, dear colleagues!

Literally an hour later. We are not afraid, even interested, if you can compare our assessment with their assessment. This is a kind of professional experience for our team of marketers who present the UAC forecast.

This year is a jubilee for UAC. We have been in existence for 10 years. We believe that we have achieved quite significant success. Starting from the fact that we have retained and developed the competence to create civil passenger aircraft. We have more than 100 SSJ 100 aircraft in operation. MS-21 has more than 175 firm orders at the moment, while still at the certification testing stage.

Also, as Mr. Masalov said, this year we signed an agreement and opened a joint venture with the Chinese aircraft manufacturing corporation COMAC in China for the full-scale launch of a program to create a wide-body family.

Over these 10 years, we have really been actively improving and developing the base and tools for creating a high-quality, sufficiently detailed and qualified market overview, its long-term forecast, precisely so that our strategic objectives, which are set within the product line, meet the market requirements that we look forward to.

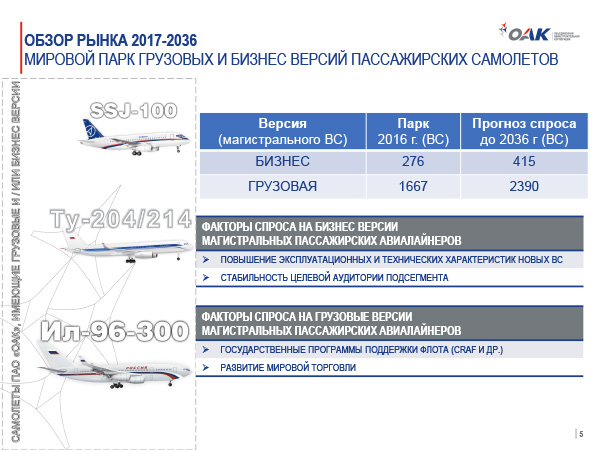

I'll start with an overview of the Russian market. In terms of the volume of the transportation market, today we occupy the 7th place in the world. We believe that by 2036 the passenger turnover of Russian airlines will grow almost 2.5 times and reach almost 500 billion passenger kilometers. At the same time, we estimate the aggregate average annual growth rate at 4.1%, which is slightly below the global average. Over the next 20 years, according to our forecast, Russian airlines will receive, based on their needs, about 1,170 new aircraft.

The existing firm orders that airlines are currently placing for various products in various categories cover about 47% of expected future demand. It should be noted that to the greatest extent this demand is covered in groups of narrow-body aircraft with a dimension of more than 120 seats. It's somewhere around 57%. Among this order, a significant share is occupied by orders for the MS-21-300 aircraft.

We also predict high demand in the segment of aircraft with a capacity of 60-120 seats, somewhere around 15% of the total demand, which is above the global average. This is primarily due to the fact that active work is currently underway, including with state support, to develop effective methods for stimulating sales, including the introduction of effective operating leasing. We are actively working with STLC to ensure that the proposals that we form are interesting and attractive to airlines.

CIS countries. We continue to classify certain countries of the region in this format, because, according to our assessment, the general problems of socio-economic development, close economic, cultural, and interpersonal ties between our countries determine precisely similar trends. Actually, mutual dependence, including that affecting the development of the market passenger traffic. According to our estimates, the volume of passenger air transportation by 2036 in the CIS countries will increase by 2.5 times. At the same time, in the global passenger turnover, passenger transportation of the countries of the CIS region is less than 1%.

We believe that, taking into account the pace of development, taking into account the stabilization of population migration, the average annual growth rate of passenger traffic in the region as a whole over 20 years will be about 4.6%. demand for new passenger aircraft in this region is approximately estimated at 260 new aircraft. Available orders currently placed cover about 18% of the estimated demand. But it should be noted that in countries this region the most active are buyers of the secondary market, where they purchase more than half of their total demand. This was taken into account in our forecast, therefore, at first glance, it may seem modest to you, but we see such predictive indicators specifically for new equipment.

China. The next most interesting for us is the Chinese market. During the forecast period, China, according to our assessment and according to the assessment of global institutions, will demonstrate the highest dynamics of development, including the dynamics of the development of passenger traffic. This will ensure the movement of China from the 4th position, from the regions we are considering, to the 3rd position, while yielding only to the countries in the aggregate of the Asia-Pacific region and Europe, and ahead of the indicators in 20 years North America and all other regions combined.

We expect passenger traffic in China to increase by more than 3.3 times over the next 20 years. Based on compound annual growth rates, we see the Chinese market could be over 6%, leading to the valuation we're showing. In 20 years, the Chinese market will require more than 7,000 aircraft. This is equivalent to $1 trillion if we evaluate this demand at catalog prices. If we talk about the portfolio of orders that Chinese airlines already have, then it covers only 19% of future demand in this market. And there is something to fight for. We estimate that the largest demand is expected in the segment of narrow-body aircraft with a capacity of more than 120 seats. At the moment, it is covered by 17% of orders, these are mostly Boeing and Airbus, as well as orders for the national Chinese project C919. We believe that, based on our current relationships and our potential development with China, we can claim a significant share in this market for the MS-21 aircraft.

Asian-Pacific area. If we talk about the Asia-Pacific region as a whole, but without China, it can be noted that, despite the relatively small excess of passenger turnover growth rates over the world average, the Asia-Pacific region will, in the forecast, take practically leading positions in the global passenger turnover market. First of all, these are: India, Malaysia, Indonesia. These countries provide the main drivers for future development, make the Asia-Pacific region the most interesting market for all manufacturers, which can transform the structure of the world park in the future.

In terms of global passenger traffic, according to our estimates, the Asia-Pacific region will occupy almost 20% of global passenger traffic by 2036. According to UAC, the total demand for new passenger aircraft in this market will be more than 8,600 units. In this case, the emphasis will be on larger aircraft. Although, if we talk about the structure of orders, at the moment, based on our forecast, the current portfolio of orders already covers 43% of the expected demand. One such significant distinguishing feature of this market should be considered that the demand for wide-body aircraft in this region will also stand out in the overall global demand, according to our estimates, it amounted to about 23%, which is slightly more than the global average.

Let's move on to the European market. For the forecast period, the European market for passenger transportation will retain its leading position in the world ranking, but it will experience quite serious competition from dynamically developing economies. First of all, this will concern long-haul transportation and the wide-body fleet. At the same time, passenger traffic will almost double. The compound annual growth rate will be 3.5%. This is lower than the world average, but this indicates that the European market has already reached a fairly serious saturation in terms of demand. Its current fleet is sizable to handle large volumes of traffic. At the same time, the share of Europe in the global passenger fleet will slightly decrease from 23% in 2016, by 2036 it will be about 19%.

European airlines are expected to purchase over 8,600 aircraft over the next 20 years. This forecast takes into account the peculiarity that the European region is the leader in the ranking of donors of the secondary market. It is renewing its fleet at an accelerated pace, transferring older aircraft to other regions. If we talk about the current portfolio of orders, it can be noted that in none of the segments in terms of capacity, the current portfolio of orders covers demand by more than 30%. Naturally, in the same region, even visually clear, there is a high share of the development of narrow-body parks. The largest share is precisely narrow-body aircraft with a capacity of more than 140 seats.

Latin America. According to our estimates, in the forecast period, the growth rate of passenger traffic in Latin America will be significantly higher than the global one, but the initially modest indicators of the total GDP in this region will rather lead to maintaining a significant distance in the total volume of passenger traffic relative to the leading regions in terms of passenger traffic.

At the same time, starting from a currently small base, we expect a threefold increase in passenger traffic at a compound annual growth rate of volumes passenger air transportation about 5.7%. But its share in the world passenger transportation market will not exceed 6.5% in 20 years. The total demand for new passenger aircraft is estimated at 3,400 aircraft. Of the announced firm orders for new aircraft, only 29% of our projected demand is covered. We expect a record high share of deliveries in the segment of narrow-body aircraft with a capacity of 120 or more seats.

Near East. Also an interesting market for UAC. Along with China and Latin America, it will significantly outpace other regions of the world in terms of growth in passenger turnover, but it is small in terms of population and has a small aggregate GDP on a global scale, which will not allow narrowing the distance between the leaders and this region.

We expect passenger traffic to grow almost 3.2 times by 2036, with a compound annual growth rate of approximately 6%. The share of the region in the total volume of passenger traffic will grow from 9.5% in 2016 to 12%. This is a big jump. It should be noted that we see more than half of new aircraft deliveries in the wide-body segment. Due to this, the share will increase to a greater extent. At the same time, 2/3 of these deliveries are expected in the segment of the group of wide-body aircraft, the capacity of which is above 320 seats. It can be said that the airlines of the region will provide up to 60% of the total global demand for these super-large aircraft.

North America. The air transportation market of the countries of the region will develop, follow the general world trends, but, taking into account the redistribution of the activity of the global economy, it will gradually lose its positions. At the turn of 2036, this market will give way not only to Europe, but also to China and the Asia-Pacific region. At the same time, the volume of passenger air transportation, according to our expectations, will almost double, with an average annual growth rate of 2.7 times.

A low rate, almost like in Europe, but this is due to the fact that a highly saturated market, initially a large current fleet structure, a fairly high rate of market saturation already now. What is important, according to our estimates, the market share of North America in the total world balance will decrease from 24% to 17%, giving way to emerging markets. A characteristic feature of the region is a high share of the expected demand for jet regional jets from 60 to 90 seats. This is about 19% of the total number of new aircraft in the region. At that time, according to the general average world indicators, this segment accounts for no more than 6%.

Africa. We note the prospects for the passenger transportation market in Africa. According to the UAC, they will be determined primarily by more than 50% increase in population over the next 20 years. In combination with rather modest indicators for the economic development of the region. The region as a whole is highly fragmented. Central and North Africa differ greatly from each other in terms of traffic indicators, in their structure of the formation of route networks. This introduces certain adjustments, which we took into account in our forecast. As a result, we give to the African market by 2036 the expectation that the volume of passenger traffic will grow by 2.5 times, with a cumulative annual rate of passenger air transportation at the level of global indicators of 4.5-4.6%. The share of the global passenger turnover market will practically not change, for 2016 it is 2.1%, for 2036 - 2.2%. African airlines, due to purchases in the secondary aircraft market, will satisfy about 41% of the total demand for passenger aircraft.

This circumstance largely determined the demand for new passenger aircraft, which is presented rather modestly. There are less than 100 aircraft for 20 years. In this situation, contrary to the current fleet structure, we see that the wide-body aircraft market promises to be the most profitable in this region. Let's just say, not by the number of seats, but by the amount of income that will come for manufacturers from the sale of this aircraft. The demand for wide-body aircraft alone is estimated by us over 20 years to be more than 200 units.

In general, if we talk about the structure of the market and demand, which we predict for a 20-year period, it can be noted that the world fleet will almost double and reach 47,000 aircraft. At the same time, it will be significantly updated, to a greater extent due to the fact that part of it will fall on the need to update the current fleet of retiring ships, part on the need associated with the development of air transportation itself.

In the current forecast 20 years, we estimate that in total across all markets, about 42,000 new passenger aircraft will be required. It is worth noting that this demand is influenced by many factors, both demand in the purely global economy and an increase in the world's population. According to estimates by national and international organizations, the population in the next 20 years will grow by more than 1.3 billion people, which will be about 20% in growth. Global GDP will grow by more than $50 trillion.

The doubling of the passenger fleet of aircraft will be influenced by changes and modernization of the existing infrastructure, the supply of more and more aircraft with new performance indicators on the market, which will lead to a reduction in the cost of transportation and an increase in the mobility of the population.

In many regions, we expect government support for airlines. There are many national programs that stimulate the development and modernization of ground infrastructure and the development of airline fleets. It is worth noting that we see the largest increase (more than 140%) in the segment of large narrow-body aircraft. This is exactly the class where the proposal for MS-21 falls.

We estimate that the fleet of narrow-body aircraft with a capacity of less than 120 seats will also almost double. As part of the implementation of the wide-body project, we see that the fleet of wide-body aircraft with a capacity of up to 300 seats will increase by more than 70%.

Thank you for your attention.